What Changed-and Why It Matters

Cash App’s fall release adds three strategic pieces: Moneybot, an AI assistant that turns account data into actionable suggestions; Lightning Network-powered Bitcoin payments you can make in USD without holding crypto; and Cash App Green, a revamped benefits program expanding eligibility and boosting APY, borrowing limits, and overdraft protection. The combined effect is to increase card spend, lower service costs, and pull crypto payments closer to mainstream checkout-all under tighter engagement incentives.

This matters because it links AI-driven financial coaching to immediate actions (split a bill, request money, check bitcoin balance), sweetens the economics for high-usage customers, and removes a key adoption hurdle for crypto payments by abstracting away custody. Block says up to 8 million accounts could qualify for new benefits-a meaningful lever on retention and interchange revenue.

Key Takeaways

- Moneybot moves beyond static dashboards to “do-something-now” prompts; early access only, with broader rollout in coming months.

- Lightning Network support lets customers pay BTC-accepting merchants in USD via QR codes, minimizing crypto custody friction.

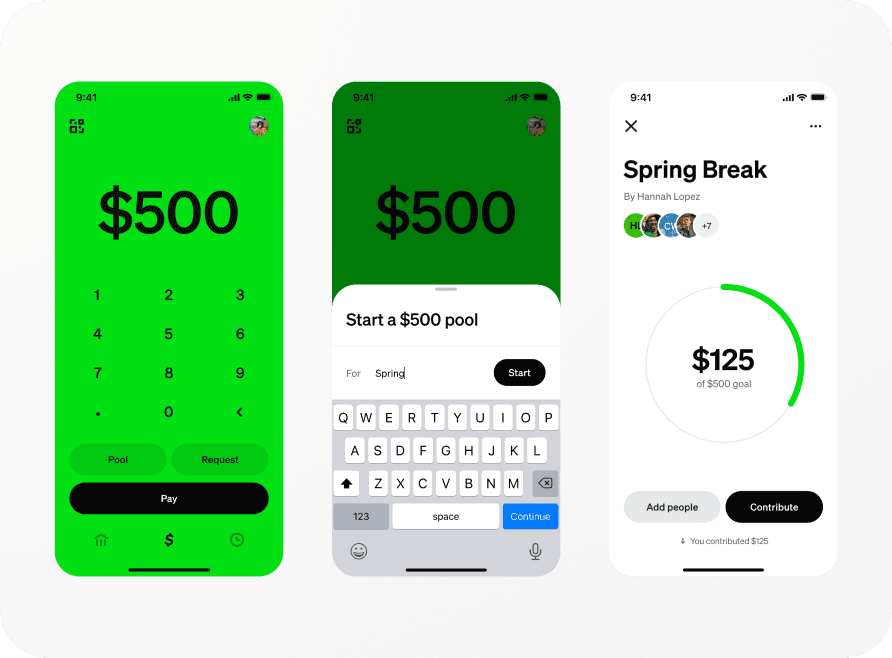

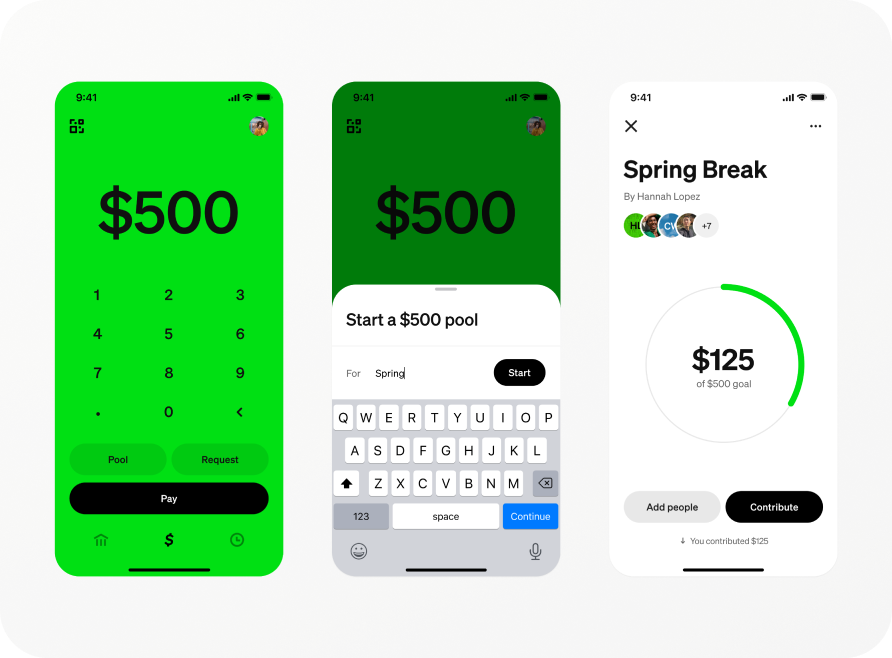

- Cash App Green widens eligibility: spend $500/month or receive $300+ in deposits to unlock benefits, potentially covering 8 million accounts.

- Benefits include up to 3.5% APY, overdraft coverage up to $200 on Card transactions, and higher Borrow limits (up to $400 for first-time borrowers).

- Borrow expands to 48 states; teen accounts get 3.5% APY with no balance cap; Afterpay features arrive inside Cash App.

Breaking Down the Announcement

Moneybot: The assistant answers questions about spending, income, and savings—e.g., “Show me my monthly income and expenses”—and surfaces tailored actions like splitting a bill or requesting money. As Cash App’s head of product design noted, the goal is to turn insights into action and adapt to each customer’s habits in real-time. Expect initial impact in support deflection and engagement: fewer taps to find information, faster task completion, and more frequent use of core features (Card, P2P, Bitcoin).

Bitcoin payments via Lightning: Customers can discover BTC-accepting merchants on a new map and pay using USD that Cash App converts over the Lightning Network. The design removes custody and volatility barriers for the average user, pushing crypto acceptance into a “tap-and-go” experience. The company says QR-based flows handle the payment. While fees on Lightning are typically low, operators should model FX spread, potential routing failures, and customer support protocols for payment exceptions.

Cash App Green program: Instead of a pure direct-deposit gate, eligibility now includes monthly spend of $500+ via Cash App Card or Cash App Pay, or deposits of at least $300. Benefits include up to 3.5% APY on savings, free in-network ATM withdrawals, overdraft coverage up to $200 on Card transactions, five weekly personalized offers, and higher Borrow limits (up to $400 for first-time borrowers, plus up to $300 increases for existing users). Block expects up to 8 million accounts to qualify.

More updates: Teen accounts get 3.5% APY with no balance cap. Borrow expands to 48 states. Afterpay (also owned by Block) integrates within Cash App for BNPL features without a separate login. The company also signaled plans to enable select customers to send and receive stablecoins in the app.

Industry Context

Fintechs are racing to package AI helpers on top of transaction data; the difference here is integration with immediate money movement and crypto rails. On APY, 3.5% is competitive but not market-leading—some consumer accounts advertise 4%+—so the real delta is in bundled benefits (overdraft, Borrow access, merchant offers) tied to usage thresholds that drive interchange and repayment revenue.

On crypto, Cash App’s USD-to-Lightning flow competes with Strike’s consumer experience and PayPal’s push into crypto payments and stablecoins. If stablecoin transfers land inside Cash App, it would close a gap with competitors leaning on USDC/PYUSD rails for low-cost, fast settlement.

Operational Considerations and Risks

- AI reliability and liability: Moneybot outputs must avoid hallucinated balances or advice. Provide explicit disclosures (not financial advice), show data sources, and log interactions for audit.

- Privacy and security: Sensitive financial data powers the assistant. Enforce strict data minimization, PCI compliance for card data, and clear opt-in/out controls for AI personalization.

- Crypto payments: Lightning routing can fail; define retry logic, timeouts, and customer recovery flows. Clarify fees, FX rates, and refund policies; volatility risk is minimized by USD conversion but not eliminated if quotes expire.

- BNPL and lending: With Borrow in 48 states and Afterpay integration, align with evolving CFPB scrutiny on fees, disclosures, and credit outcomes. Monitor delinquency and roll rates by segment.

- Overdraft features: Free coverage up to $200 increases satisfaction but adds risk cost. Implement guardrails based on income regularity and recent balance volatility.

What This Changes for Operators

The release tightens the loop from insight to action: AI prompts trigger money movement, benefits nudge higher monthly engagement, and crypto rails become an invisible utility rather than a hobbyist feature. For merchants in Square’s ecosystem, easier Bitcoin acceptance via Lightning plus Cash App’s discovery map could lift alternative tender share without pushing crypto custody onto consumers.

The bigger strategic play is wallet primacy. By loosening eligibility from direct deposit to either spend or deposits, Cash App can convert casual users into primary or secondary wallet status and monetize via interchange, lending, and cross-sell—while the assistant lowers friction and support load.

Recommendations

- Product leaders: Instrument Moneybot with task-completion metrics (bill split initiated, transfer executed, dispute started) and AB-test prompts tied to measurable financial outcomes, not engagement vanity metrics.

- Risk and compliance: Implement pre-release red teaming for the assistant; require source-of-truth callouts in responses; store immutable chat logs for supervisory review. Refresh crypto disclosures and complaint handling specific to Lightning payments.

- Growth and lifecycle teams: Use Cash App Green as a laddered program—progressive offers that move users from P2P-only to Card spend to savings and Borrow. Track lift in monthly active spenders and benefit cost per incremental dollar of interchange.

- Engineering/ops: Build failover paths for Lightning (fallback to on-chain or void), clear refund SLAs, and transparent FX/fee displays. For BNPL and Borrow, tighten risk models for teens and new-to-credit cohorts, with real-time affordability checks.

Bottom line: The AI assistant is the hook, but the benefits redesign and crypto payment abstraction are the revenue engines. If executed with strong guardrails, this release can deepen wallet share while keeping compliance risk manageable.