Executive summary — what changed and why it matters

Harbinger’s November 2025 acquisition of Phantom AI signals a structural shift: the electric truck maker is evolving from a chassis-only supplier into an integrated hardware-software provider with a new software licensing revenue stream, pending Tier-1 OEM rollouts.

Thesis: The deal repositions Harbinger as a combined chassis and software vendor, creating its first recurring software income channel through Tier-1 partnerships rather than a one-off EV hardware play.

Key takeaways

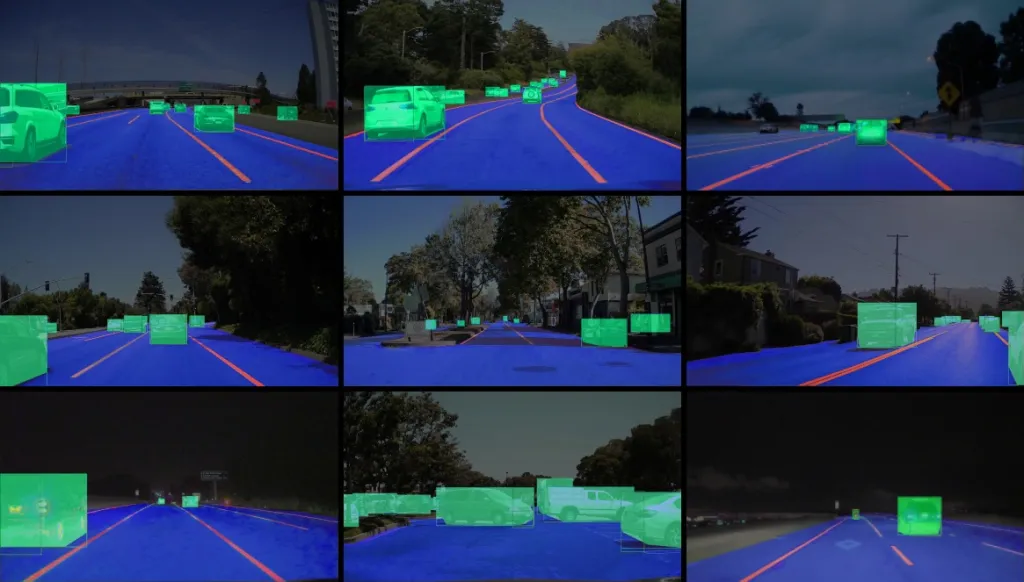

- Structural shift: Harbinger moves from chassis-only to integrated supplier by folding Phantom’s Level-2 computer-vision ADAS team into its platform and licensing that software via ZF Group.

- Quantified impact: Phantom’s 30-person autonomy group joins Harbinger’s recently raised $160 million war chest; Harbinger projects “millions” in software revenue in 2026, according to CEO John Harris, with scale hinging on ZF/OEM rollouts in 2027-28.

- Operational advantage: Embedding automatic emergency braking, adaptive cruise control, lane keeping and backup cameras addresses safety gaps in medium-duty fleets and could reduce low-speed collision costs.

- Persistent hurdles: Regulatory certification, third-party liability and integration complexity with vehicle electronics and telematics remain significant obstacles.

Breaking down the announcement

The acquisition, closed in November 2025 and publicized in February 2026, folds Phantom AI’s Level-2 computer-vision stack into Harbinger’s medium-duty electric chassis. Harbinger says it had been field-testing Phantom’s ADAS pre-acquisition and will deepen integration to standardize features such as virtual bumpers, acoustic alerts, automatic emergency braking (AEB), adaptive cruise control and lane keeping.

Concurrently, Harbinger licensed the same ADAS software to Tier-1 supplier ZF Group for packaging and sale into passenger-car OEM channels. This marks Harbinger’s first venture into software services revenue, complementing its January 2026 expansion into battery-pack sales and a $160 million funding round co-led by FedEx and THOR Industries.

Why this matters for operators and buyers

Fleet operators are likely to see enhanced safety in medium-duty EVs as Level-2 ADAS fills gaps in legacy trucks commonly used in depots and urban routes, which could translate into lower downtime and repair outlays. For Harbinger, the move embeds differentiated software under its chassis brand, offering exposure to higher-margin, recurring licensing fees if ZF’s OEM channels gain traction.

Competitors and alternatives

Harbinger’s path to ADAS contrasts with aftermarket retrofit players and established software-hardware stacks. Mobileye leads vision-based ADAS for OEMs; Nvidia offers full compute platforms and Drive software; Aurora and Waymo push into freight autonomy. Harbinger’s chassis ownership and direct embedding of Phantom’s vision-first Level-2 system—combined with a ZF partnership—provides an integrated OEM channel versus retrofit or third-party stack licensing.

Risks, governance and regulatory considerations

Licensing and deploying Level-2 ADAS across vehicle classes raises questions around FMVSS and NHTSA compliance in the U.S., UNECE regulations abroad, and liability frameworks for third-party software failures. Over-the-air update governance, telematics data privacy and post-deployment safety monitoring also present governance challenges. Insurers and fleet customers will seek documented performance metrics and robust validation records.

What to watch next

- ZF’s deployment timeline and any OEM integration announcements through 2028, which will drive software licensing revenue scale.

- Third-party safety validations or pilot data published after Harbinger truck demos at fleet expos.

- Regulatory filings, field safety notices or recalls related to the integrated ADAS solution.

- Signals from Harbinger on roadmaps beyond Level-2 toward higher autonomy tiers.

Implications for stakeholders

- Fleet operators: Early deployments of integrated ADAS may offer measurable reductions in low-speed collisions and downtime, shaping future procurement choices around safety features.

- OEMs and Tier-1 suppliers: The Harbinger/ZF licensing model will factor into integration roadmaps as stakeholders evaluate transparency of software validation, update cadences and liability frameworks.

- Insurers and risk teams: Premium models for medium-duty EVs are likely to be reassessed in light of factory-integrated ADAS, with a premium on third-party performance data.

- Investors and partners: ZF’s OEM traction and emerging software margin trends will serve as key indicators of recurring revenue viability and multi-year adoption risk.